There is a significant case for loyalty to be considered a financial asset by organization. At first, it appears to be a liability, but on closer inspection this is clearly not the case.

In this post, Pointsville Research dives into the compelling use cases that prove that loyalty is not only an asset, but an one that can be rightfully considered alongside other alternative assets.

How Airlines Leveraged Loyalty as an Asset

Source: Willy Wo, Unsplash

Not surprisingly, airlines were the first organizations to utilize loyalty as an asset to collateralize for business operations. After all, these were the first organizations to incorporate loyalty into their business model. You can read this post for more details on the history of loyalty.

In 2020, during the COVID-19 pandemic airlines faced a crisis. Several airlines were able to generate an infusion of significant capital by borrowing against their loyalty program.

This use case was proof that customer loyalty is an asset, and one that can be successfully collateralized.

American Airlines Loyalty

In March 2021, American Airlines Group Inc. (NASDAQ: AAL) successfully concluded a $10 billion financing arrangement secured by its AAdvantage® program, which also led to the prepayment of its secured loan from the U.S. Department of the Treasury, effectively ending its commitments under the loan agreement.

In September 2020, the company had borrowed $550 from the US Treasury Department. As of March 2021, American had fully repaid the $550 million loan and terminated its loan agreement with the government.

United Airlines Loyalty

In June 2020, United Airlines (NASDAQ: UAL) announced it had secured a $5 billion loan by using its MileagePlus loyalty program as collateral, aimed at navigating through the challenges posed by the coronavirus pandemic.

The move was part of United’s strategy to amass a $17 billion cash reserve by the end of the third quarter, aiming to triple their typical liquidity level. The MileagePlus program, a critical asset generating $5.3 billion in annual cash flow and $1.8 billion in EBITDA profit, valued at an estimated $20 billion, underpinned this loan. Listed accured revenue included: including frequent flier mile redemption for flights, credit card spending, and partnerships with hotels and car rental services.

The loan was provided by Goldman Sachs, Barclays Bank, and Morgan Stanley and ensured the company to retain full operational control and did not relinquish any equity.

Delta Airlines Loyalty

In September 2020, Delta (NASDAQ: DAL) borrowed $9 billion, after originally announcing a $6.5 billion raise as it was oversubscribed. This is significant as it was over 40% of their market cap at the time.

The debt deal backed by its frequent flyer program, SkyMiles, rather than seek a government loan.

This financing was done to mitigate the impacts of the travel downturn and included a $6 billion private offering, secured by Delta’s SkyMiles program, and was divided into two parts: $2.5 billion in senior secured notes at 4.5% due in 2025, and $3.5 billion in senior secured notes at 4.75% due in 2028, both of which were oversubscribed with $16 billion worth of orders.

Additionally, Delta secured a $3 billion institutional loan, which was also oversubscribed with offers of $10 billion, marking the airline industry’s largest fundraising transaction to date.

Loyalty is an Untapped Asset

This financial strategy reflected a broader industry trend where airlines, facing a crisis, successfully leveraged their frequent flyer programs for capital. Frequent flyer programs, such as Delta’s SkyMiles with its 92 million members, had proven to be resilient profit centers, maintaining revenue flow through credit card and bank partnerships despite a decrease in passenger revenue.

This actions demonstrated the strategic importance of loyalty programs and their value as an economic asset.

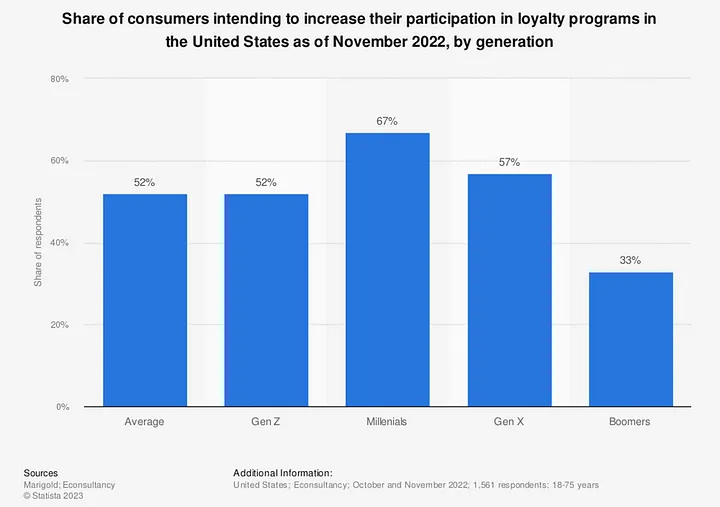

This is true of other loyalty programs and industries as well. In fact, more than half of American consumers plan to increase their participation in loyalty programs.

Source: Pointsville Research

New generations are inheriting global wealth and they are focused on alternative assets.

Millennials and Gen X are most active in loyalty programs as well as being the most active investors over the next decade. Thus loyalty has a rock-solid case for being included among other alternative investments.

About Pointsville

At Pointsville, we are dedicated to building an alternative asset factory. We see multi-billion dollar opportunity in the loyalty asset sector.

Pointsville is a leader in loyalty and alternative asset digitization, operating as a comprehensive platform offering best-in-class loyalty, capital markets, regulatory, blockchain and other tools and products.

Contact us at partner@pointsville.com or connect with us across social media.